HSA 2026: Maximize Your $4,100 Triple Tax Advantage

Health Savings Accounts (HSAs) in 2026 offer an unparalleled triple tax advantage for eligible individuals, allowing tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses, with a new individual contribution limit of $4,100.

Understanding and leveraging the benefits of Health Savings Accounts (HSAs) in 2026: Maximizing Your Triple Tax Advantage with a $4,100 Contribution Limit is more crucial than ever for Americans seeking to optimize their healthcare and financial futures. These powerful accounts offer a unique opportunity to save, invest, and spend on medical expenses with significant tax benefits. As the healthcare landscape evolves, mastering your HSA can be a game-changer for both immediate needs and long-term financial security.

The foundation of HSAs: Eligibility and basic structure

Health Savings Accounts (HSAs) are not for everyone, but for those who qualify, they represent a cornerstone of smart financial planning. Eligibility hinges on your health insurance plan; you must be enrolled in a High-Deductible Health Plan (HDHP) and not be covered by any other non-HDHP health insurance, nor be enrolled in Medicare, nor be claimed as a dependent on someone else’s tax return. This fundamental requirement ensures that HSAs are primarily utilized by individuals who take on more direct responsibility for their initial healthcare costs.

Once eligible, an HSA functions much like a personal savings account, but with significant tax advantages. Contributions can be made by you, your employer, or both, up to the annual limit. For 2026, this limit is notably set at $4,100 for individuals, with an additional catch-up contribution for those aged 55 and over. These funds are specifically designated for qualified medical expenses, but their utility extends far beyond simple reimbursement.

Understanding HDHPs

High-Deductible Health Plans are characterized by higher deductibles than traditional insurance plans. In return, they typically offer lower monthly premiums. For an HDHP to be HSA-eligible in 2026, it must meet specific criteria for minimum deductibles and maximum out-of-pocket expenses. This structure encourages participants to be more mindful of their healthcare spending.

- Lower monthly premiums compared to traditional plans.

- Higher deductibles that must be met before insurance coverage kicks in.

- Requires careful budgeting for potential out-of-pocket medical costs.

The synergy between an HDHP and an HSA is critical. The HDHP provides catastrophic coverage, while the HSA acts as a tax-advantaged vehicle to cover the deductible and other qualified medical expenses. This pairing empowers individuals to manage their health finances proactively, fostering a sense of control over their healthcare expenditures.

In essence, establishing eligibility and understanding the basic structure of an HSA is the first step toward unlocking its profound financial benefits. It’s about recognizing that an HDHP isn’t just a cost-saving measure on premiums, but a gateway to a powerful savings and investment tool.

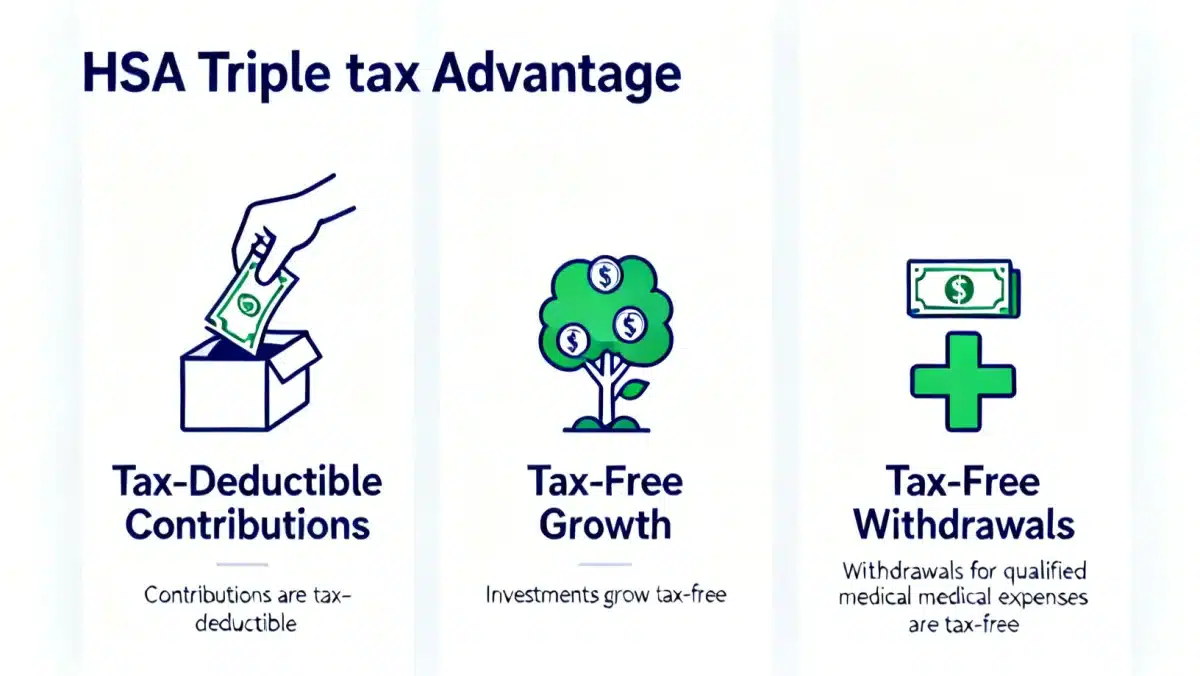

Unpacking the triple tax advantage for 2026

The allure of an HSA lies primarily in its unique triple tax advantage, a feature almost unparalleled in the financial world. This advantage makes HSAs incredibly powerful for both immediate healthcare costs and long-term financial planning. Understanding each component is key to maximizing its benefits, especially with the individual contribution limit reaching $4,100 in 2026.

The first pillar is tax-deductible contributions. Every dollar you contribute to your HSA, up to the annual limit, is tax-deductible. This means you reduce your taxable income for the year, potentially lowering your overall tax bill. If your employer contributes on your behalf, those contributions are also tax-free to you, adding to the immediate savings.

The second pillar involves tax-free growth. Once funds are in your HSA, they can be invested, much like a 401(k) or IRA. Any earnings from these investments—whether through interest, dividends, or capital gains—grow tax-free. This compounding growth over time can significantly boost the value of your account, turning your HSA into a formidable investment vehicle.

The power of tax-free withdrawals

The third, and arguably most significant, pillar is tax-free withdrawals for qualified medical expenses. When you use your HSA funds to pay for eligible medical costs, those withdrawals are completely tax-free. This includes a wide range of expenses, from doctor visits and prescriptions to dental care, vision care, and even certain long-term care insurance premiums. This tax-free withdrawal feature ensures that every dollar saved and grown within your HSA retains its full purchasing power for healthcare needs.

- Contributions reduce taxable income.

- Investment earnings grow without being taxed.

- Withdrawals for qualified medical expenses are tax-free.

This triple advantage creates a highly efficient financial tool. Instead of paying for medical expenses with after-tax dollars, you’re using pre-tax contributions that have grown tax-free, and are withdrawn tax-free. This effectively means you get a discount on your healthcare costs, making your money work harder for you. Beyond medical expenses, after age 65, HSA funds can be withdrawn for any purpose without penalty, though they will be taxed as ordinary income if not used for qualified medical expenses, similar to a traditional IRA. This flexibility further solidifies the HSA’s role in comprehensive financial planning.

Strategic contributions: Reaching the $4,100 limit in 2026

For 2026, the individual contribution limit for Health Savings Accounts has increased to $4,100, presenting an even greater opportunity for eligible individuals to maximize their triple tax advantage. Strategically contributing to your HSA means more than just hitting the limit; it involves understanding how to make the most of this powerful savings vehicle. Whether you contribute through payroll deductions or directly, consistency and planning are key to reaching this enhanced threshold.

Many employers offer payroll deductions for HSA contributions, which is often the easiest and most effective way to contribute. These contributions are typically made pre-tax, meaning they reduce your gross income before federal income tax, and often state income tax (depending on your state’s laws) and FICA taxes are calculated. This immediate tax saving is a significant benefit, effectively providing a discount on your contributions from the start.

Catch-up contributions for those 55 and over

Individuals aged 55 and older have an additional advantage: they can make catch-up contributions. For 2026, this additional contribution amount remains consistent with previous years, allowing those nearing retirement to further bolster their healthcare savings. This provision acknowledges that healthcare costs often increase with age, providing a crucial mechanism for older individuals to prepare.

- Contribute through pre-tax payroll deductions for immediate savings.

- Consider making a lump sum contribution if you have available funds.

- Utilize catch-up contributions if you are 55 or older to add extra funds.

For those who don’t have employer-sponsored payroll deductions, direct contributions are also fully tax-deductible. It’s important to keep accurate records of these contributions for tax purposes. Even if you can’t contribute the full $4,100 immediately, starting with a manageable amount and gradually increasing it throughout the year can help you reach your goal. The goal is not just to save, but to strategically leverage the tax benefits that come with each dollar contributed, setting yourself up for long-term financial health and security.

Investing HSA funds for long-term growth

While HSAs are primarily known for their tax advantages on contributions and withdrawals for medical expenses, their true power as a financial tool is unlocked when you invest the funds for long-term growth. Many HSA providers offer investment options, allowing your money to grow tax-free, similar to a 401(k) or IRA. This makes your HSA not just a savings account for current medical bills, but a robust retirement savings vehicle.

To effectively invest your HSA funds, it’s often recommended to maintain a certain amount of cash in your account for immediate medical needs. This liquid portion ensures you can cover unexpected expenses without having to sell investments at an inopportune time. The remaining funds can then be allocated to various investment options, such as mutual funds, exchange-traded funds (ETFs), or individual stocks, depending on your risk tolerance and financial goals.

Choosing the right investment strategy

Selecting the right investment strategy for your HSA involves considering your time horizon and comfort with risk. If retirement is decades away, you might opt for a more aggressive portfolio focused on growth stocks. If you’re closer to retirement, a more conservative approach with a mix of bonds and stable equities might be more suitable. The key is to align your HSA investment strategy with your broader financial plan.

- Determine a cash reserve for immediate medical expenses.

- Research investment options offered by your HSA provider.

- Diversify your investment portfolio based on your risk tolerance.

The tax-free growth within an HSA means that over decades, even modest contributions can accumulate into a substantial sum. This growth, combined with the ability to withdraw funds tax-free for qualified medical expenses at any age, makes investing your HSA an intelligent strategy. For those who manage to pay for current medical expenses out-of-pocket and allow their HSA to grow, it essentially becomes a supplemental retirement account, offering unparalleled flexibility to cover future healthcare costs, which can be significant in retirement.

Qualified medical expenses: What you can pay for

One of the most attractive features of an HSA is the ability to withdraw funds tax-free for qualified medical expenses. Understanding what constitutes a qualified expense is crucial to fully leveraging this benefit without incurring penalties or taxes. The IRS defines a broad range of expenses that are considered qualified, providing extensive coverage for healthcare needs.

Generally, qualified medical expenses include amounts paid for the diagnosis, cure, mitigation, treatment, or prevention of disease, and for treatments affecting any structure or function of the body. This encompasses a wide array of services and products, from prescription medications and doctor visits to dental care, vision care, and even certain over-the-counter items prescribed by a physician. It’s important to note that expenses must be primarily for the prevention or alleviation of a physical or mental defect or illness.

Common qualified expenses

The list of qualified medical expenses is extensive and can sometimes be surprising. Beyond the obvious, like hospital stays and surgical procedures, it includes less conventional items. For example, acupuncture, chiropractic care, and even certain weight-loss programs prescribed by a doctor for a specific medical condition can be covered. Premiums for long-term care insurance, Medicare Part B and D, and Medicare Advantage plans also qualify, making HSAs particularly valuable in retirement.

- Doctor’s visits, hospital stays, and prescription medications.

- Dental care, including cleanings, fillings, and orthodontia.

- Vision care, including eye exams, glasses, contact lenses, and even laser eye surgery.

- Mental health services, physical therapy, and other specialized treatments.

Keeping meticulous records of your medical expenses is vital. While you don’t typically need to submit receipts to your HSA administrator for each withdrawal, the IRS may request documentation in an audit. Therefore, maintaining organized records ensures you can justify tax-free distributions. This careful approach protects your triple tax advantage and ensures you are fully compliant with IRS regulations, allowing you to confidently utilize your HSA for all your qualified healthcare needs.

HSA as a retirement planning tool

While often viewed as a healthcare savings account, an HSA truly shines as a powerful, often underestimated, retirement planning tool. Its unique tax advantages, particularly the ability for funds to grow tax-free and be withdrawn tax-free for qualified medical expenses, make it an ideal complement to traditional retirement accounts like 401(k)s and IRAs. For many, healthcare costs in retirement can be a significant financial burden, and an HSA provides a dedicated, tax-efficient way to address this.

The key to using an HSA for retirement is to treat it less like a checking account for immediate medical bills and more like an investment account. If you have the financial capacity, try to pay for current medical expenses out-of-pocket and allow your HSA funds to remain invested and grow. By doing so, you’re building a substantial nest egg specifically earmarked for future healthcare costs, which can be substantial.

The age 65 flexibility

Upon reaching age 65, the flexibility of an HSA expands significantly. At this point, you can withdraw funds for any purpose without penalty. If the withdrawals are still for qualified medical expenses, they remain tax-free. If used for non-medical expenses, they are taxed as ordinary income, similar to withdrawals from a traditional IRA or 401(k). This gives you incredible flexibility: tax-free for healthcare, or a supplemental income stream if healthcare costs are lower than anticipated.

- Invest HSA funds aggressively if you can cover current medical costs out-of-pocket.

- Recognize it as a long-term investment vehicle for future healthcare needs.

- Leverage the age 65 rule for penalty-free withdrawals, medical or otherwise.

The long-term compounding growth within an HSA, combined with its tax-free nature, can lead to significant savings. Imagine decades of tax-free growth on contributions up to the $4,100 limit, plus catch-up contributions if eligible. This can create a formidable fund to cover deductibles, copayments, and even Medicare premiums in retirement, ensuring your golden years are not overshadowed by medical bills. For those who prioritize contributing the maximum to their HSA, it becomes a strategic pillar in a robust retirement strategy, offering peace of mind and financial security.

Maximizing your HSA: Advanced strategies and considerations

Beyond simply contributing the maximum allowable amount, there are several advanced strategies and considerations that can help you truly maximize the benefits of your Health Savings Account. These strategies focus on optimizing your contributions, managing your investments, and leveraging the account for long-term financial health, especially with the 2026 individual contribution limit at $4,100.

One powerful strategy is to pay for current medical expenses out-of-pocket and save your receipts. The IRS allows you to reimburse yourself for past qualified medical expenses at any point in the future, as long as the expense was incurred after your HSA was established. This means you can let your HSA investments grow tax-free for years, or even decades, and then take a tax-free distribution to reimburse yourself for those accumulated expenses when you need the cash most, perhaps in retirement.

Considerations for switching health plans

It’s crucial to understand the implications if you switch from an HDHP to a non-HDHP, or enroll in Medicare. While you won’t be able to contribute new funds to your HSA, your existing HSA funds remain yours to use for qualified medical expenses, and they continue to grow tax-free. This portability is a significant advantage, ensuring that your accumulated savings are never lost, regardless of changes in your health insurance coverage.

- Pay current medical expenses out-of-pocket and save receipts for future reimbursement.

- Understand that HSA funds are portable, even if you lose HDHP eligibility.

- Review your HSA investment options regularly and adjust as needed.

Another consideration is to carefully choose your HSA provider. While many employers offer a default option, you might have the flexibility to transfer your funds to a different HSA custodian that offers better investment options, lower fees, or more user-friendly services. Regularly reviewing your HSA’s performance and fees ensures you’re getting the most out of your account. By adopting these advanced strategies, an HSA transforms from a simple savings account into a dynamic financial tool, capable of significantly bolstering your financial well-being throughout your life and into retirement.

| Key Point | Brief Description |

|---|---|

| 2026 Contribution Limit | Individuals can contribute up to $4,100, a significant increase for healthcare savings. |

| Triple Tax Advantage | Contributions are tax-deductible, growth is tax-free, and qualified withdrawals are tax-free. |

| Investment Potential | Funds can be invested for long-term, tax-free growth, acting as a retirement savings tool. |

| Retirement Flexibility | After age 65, funds can be withdrawn penalty-free for any purpose (taxable if not medical). |

Frequently asked questions about HSAs in 2026

For 2026, the individual contribution limit for Health Savings Accounts is $4,100. This amount represents a significant increase, allowing individuals to save even more for qualified medical expenses with substantial tax advantages.

To be eligible, you must be enrolled in a High-Deductible Health Plan (HDHP) and have no other disqualifying health coverage. You cannot be enrolled in Medicare or be claimed as a dependent on someone else’s tax return.

The triple tax advantage includes tax-deductible contributions, tax-free growth on investments, and tax-free withdrawals for qualified medical expenses. This makes HSAs incredibly efficient for healthcare savings and retirement planning.

Yes, after reaching age 65, you can withdraw HSA funds for any purpose without penalty. However, if the withdrawals are not for qualified medical expenses, they will be taxed as ordinary income, similar to a traditional IRA withdrawal.

For long-term growth and retirement planning, investing your HSA funds is highly recommended. Keep a portion as cash for immediate needs, but allow the rest to grow tax-free through various investment options offered by your HSA provider.

Conclusion

The Health Savings Account in 2026, with its enhanced $4,100 individual contribution limit, stands as an indispensable financial tool for eligible Americans. Its unparalleled triple tax advantage—tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses—offers a unique pathway to both manage current healthcare costs and build substantial wealth for retirement. By strategically contributing, investing wisely, and understanding the breadth of qualified expenses, individuals can truly maximize their HSA’s potential. This powerful account is more than just a savings vehicle; it’s a cornerstone of comprehensive financial planning, providing flexibility, security, and significant tax benefits for years to come.